Example Regulatory Reporting Scheme Working Prototype: Common Elements of Financial Report

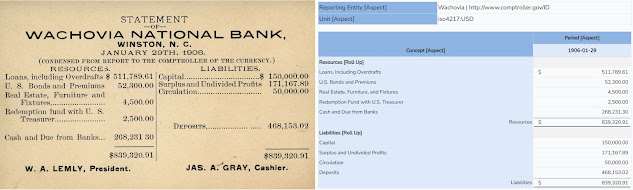

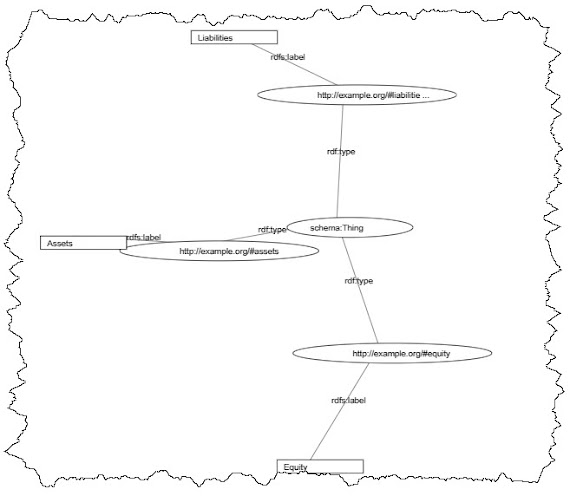

This blog post explains a completely new approach to regulatory reporting. This prototype uses a very basic, simple example of a reporting scheme to keep this first example easy to explain. See the "Additional Information" section below for more sophisticated report fragments. This regulatory reporting scheme is created using the Seattle Method framework. To test the framework I created about 35 different reporting schemes. Here is the list which contains pointers to all reporting scheme metadata . Those 35 different reporting schemes were used to test the framework. For this demonstration I will use the Common Elements of Financial Statement (Version 3) (Four Statement Model) prototype financial reporting scheme. Imagine that as an example of a regulator reporting scheme. Step 1 would be for a regulator to create and publish their reporting scheme using the XBRL global standard following the good practices specified by the Seattle Method. That includes ...