Becoming an Expert in XBRL-based Reporting

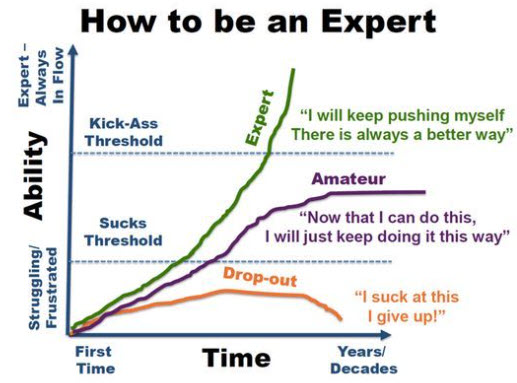

Practice does not make perfect; perfect practice makes perfect. What I am trying to point out with that statement is that doing the wrong things over, and over, and over again to get your "10,000 hours" in does not make you an expert. Doing the right things the right way makes you an expert. The world is pivoting, a transition is occurring. My take on that transition is articulated in my document The Great Transmutation . You can believe my view of the world or not. If you are a believer then it might seem apparent that we need more people that understand how to do XBRL-based digital financial reporting appropriately. Marcus Köhnlein posted information on LinkedIn, How to become an expert , that provides general information about how to become an expert in some field and this helpful graphic: Here is the general, detailed list from that post above. That is a decent list. I don't think that there is a specific ordering to the list. Identify what you're...