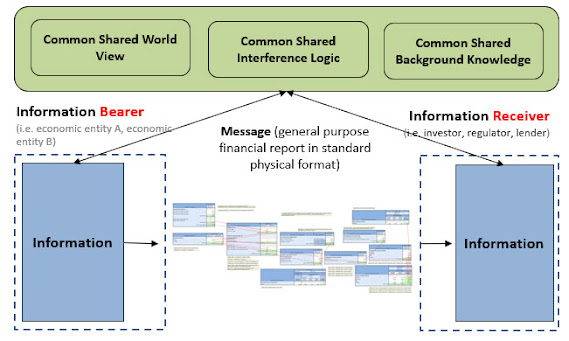

Using Rules to Eliminate Blind Spots

A system is in effect “blind” to things not covered by that systems rules. In the past I have said a similar sort of thing by explaining that rules provide "guardrails" or "bumpers" or "guiderails". The following graphic helps one understand the value of the Standard Business Report Model (SBRM) and the guidance of the Seattle Method . On the LEFT are the “pillars of quality” that the FASB and SEC seem to be currently relying on: the XBRL technical syntax and some rules about the math in a report that tends to not be enforced. On the RIGHT is how my Seattle Method sees a financial report and how I hope SBRM sees financial reports and business reports. Again I say: A system is in effect “blind” to things not covered by that systems rules . ( Click here for larger image ) Think about that statement a minute. What exactly, if not system rules, is the software system relying on in order to understand information if not for the rules of the system? Magic?...