The average accountant is, well..., average. Precision is the difference between a professional and a dilettante.

The Decision Lab article, Why can we not perceive our own abilities?, points out the phenomenon by which those least competent in a certain subject area overestimate their skills the most and that those most competent in a subject area to think less of their own talents. This phenomenon is referred to as The Dunning-Kruger effect.

Another way of understanding this notion that the average accountant is average is by considering the normal distribution. This is also often called the "bell shaped curve". Normal distributions or bell shaped curves are very common in nature. While the actual shape of the bell shaped curve can vary based on the variability or standard deviation around the mean; the shapes tend to be in the form of a "bell" shaped pattern:

This version of a graphic of a normal distribution helps one understand that about 50% of people tend to meet expectations, 15% are above expectations, 15% are below expectations, 10% have serious under performance issues, and 10% are stars and have excellent performance:

Financial accounting and financial reporting are areas of knowledge. There is a tool called the

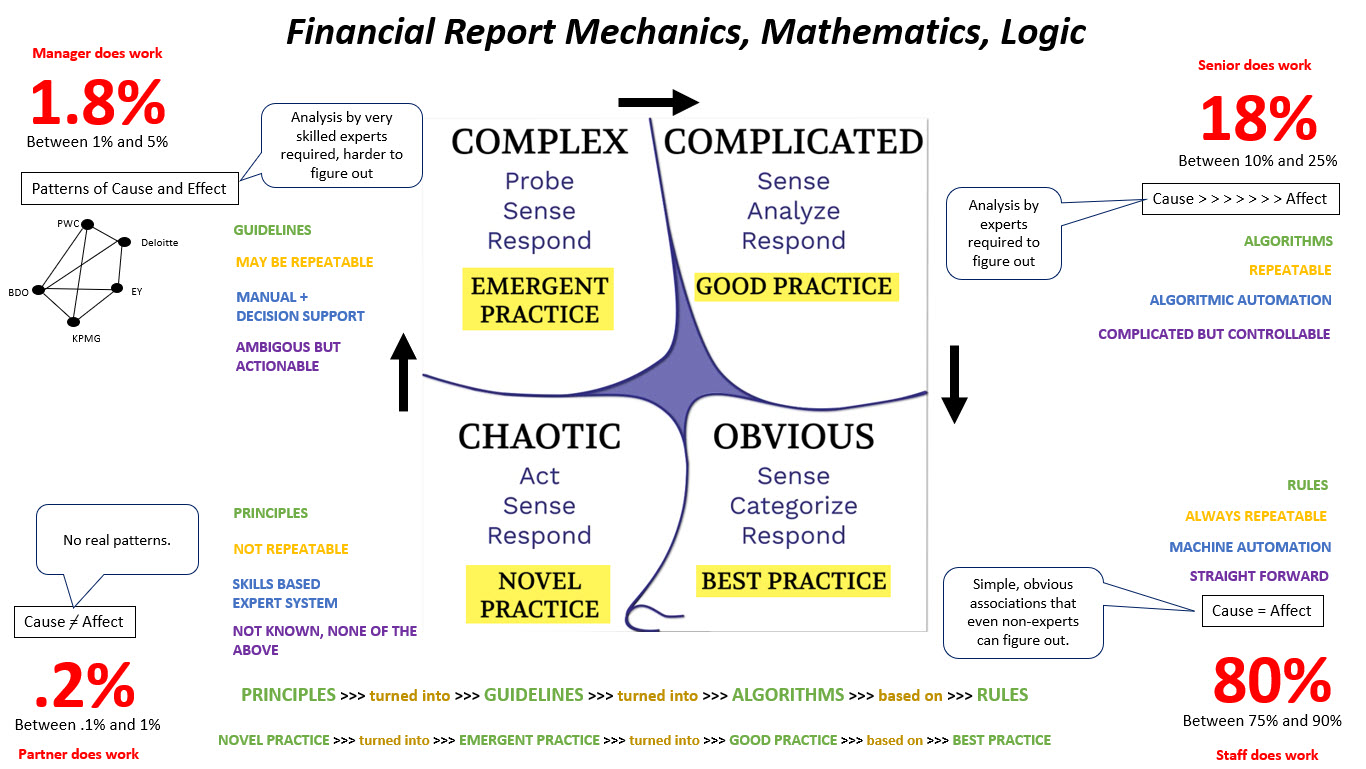

Cynefin Framework for understanding the complexity within an area of knowledge. This YouTube video,

Complexity, Cynefin, and Agile, does an excellent job of explaining the ideas behind the Cynefin Framework. There are

many different types of approaches for making sense of an area of knowledge.

My analysis of the financial reporting area of knowledge

focusing specifically on the logical, mathematical, and mechanical characteristics of the financial report itself have helped me understand the patterns of a financial report.

What I mean by that is that this does NOT INCLUDE the "measurement" and "recognition" and "matching" and "materiality" and "alternative approaches" allowed which related to judgment and are subjective in nature; I stayed in the area that is completely objective and are more science and math that the judgement related aspects that are related to the

principles of accounting and reporting. My focus is the REPORT ITSELF once an accountant has determined, using judgment, the things that go into the report.

Fitting an area of knowledge into groups is possible because of patterns. If you have the skill of advanced

pattern recognition, as I seem to have, seeing the patterns is easy. There are many pattern recognition techniques: templates matching, prototype matching, feature analysis, components theory.

- There are obvious best practices for about 80% of the mechanical aspects of a financial report.

- There are pretty obvious good practices for another 18% of the mechanical aspects of a financial report.

- There are some more complex aspects of the mechanics of creating a report where, say, different CPA firms might even disagree; but within a CPA firm or within some "group" (say a specific partner), they are sure of what the right answer to a complex issue is, those complex aspects make up about 1.8% of a financial report.

- Finally, not so obvious novel practice makes up another .2% of the mechanical aspects of creating a financial report.

And I will say this in yet another way, helping the reader understand how accounting and reporting issues can be stratified. A collogue of mine works for one of the Big 4 professional services firms. What he does is provide "level 4" support for "complex" and/or "unique" accounting and reporting issues and situations.

My friend is supposed to deal with only the most “complex” and “unique” accounting and reporting issues that are escalated to him as a professional services consultant to be dealt with. That consultant is like “level 4” technical support where “level 1” tend to be dealt with by the individual accountant performing work, “level 2” might be escalated to the senior accountant on the project, “level 3” might be escalated to the accounting manager or audit partner that is in charge of the reporting engagement.

The point that I am trying to make is that the percentages you see above (the 80%, 18%, 1.8%, and .2%) are NOT THE COMPLETE SET OF ISSUES escalated to “level 4” for resolution. My friend ONLY deals with the most complex and unique (i.e. novel) accounting and reporting issues.

Another breakdown of those four categories above (best practice, good practice, emergent practice, and novel practice) might be something like:

- OBVIOUS: A very significant part (say 98%, this tends not to be escalated) of financial accounting and reporting issues are "obvious" and "best practices" exist and they are rarely, if ever, escalated to "level 4" support. These issues can be easily addressed by an accountant that has a college degree in accounting, has passed the CPA or CA licensing examination, has worked in accounting for a couple of years, and understands how to read the financial reporting standards and available interpretations of those standards, and otherwise has the SKILLS and EXPERIENCE to address the specific issue. And, those skills and experience are either:

- Applied correctly due to appropriate accounting skills and experience or;

- Applied incorrectly do to some mismatch between the skills and experience necessary and the skills and experience of the accountant performing the work.

- COMPLICATED: A very small part (say 2%, this is what is escalated to "level 4" support) of financial accounting and reporting issues are more "complicated" and "good practices" can be applied to addressing any issues because of poorly stated accounting standards which instantiate themselves as specific ambiguities within the standards, specific conflicts within the standards, or specific contradictions within the standards. And accountants bring their SKILLS and EXPERIENCE to the accounting or reporting situation and either:

- Apply their judgement sensibly to arrive at a sensible outcome for the issue or;

- Apply their judgement incorrectly to arrive at an inappropriate outcome.

- COMPLEX (EMERGENT): New type of specific accounting transaction or specific reporting and/or complexity of a specific existing type of accounting transaction or reporting issue.

- Apply judgement sensibly and leveraging specific interpretations (step above) to arrive at a sensible outcome.

- Apply judgement incorrectly and leveraging specific interpretations to arrive at an inappropriate outcome.

- CHAOTIC (NOVEL): New type of general accounting transaction or general reporting and/or complexity.

The moving pieces of the puzzle of digital financial reporting involves putting those pieces together correctly and effectively. But I think that we can agree with the following:

- Accountants do not have the same skill levels. Some are really good, some are really bad, and most are only average.

- Accounting and reporting standards/rules are not perfect (frustratingly poor at times). Ambiguity exists within standards, inconsistencies exist, contradictions exist.

- Both “objective stuff” (very obvious, everyone pretty much agrees) and “subjective stuff” (requires professional judgement) exists in financial reporting.

- New stuff (e.g., no accounting standards exist yet) and new complexities to existing stuff (e.g., no accounting standards exist yet) pops up from time-to-time and will continue to pop up pretty much forever.

- It is really hard to figure out “new stuff” and “new complexities to existing stuff” if the foundational accounting/reporting standards are frustratingly poor. This requires the best professional judgement.

- Because accounting standards (all of them) can sometimes be “frustratingly poor”; it can be even harder to figure out how to handle the “new stuff” and “new complexities to existing stuff”.

- Given all of the above, the highest value that an accountant can provide given all of the above is to have the skills and experience to overcome the complexities caused by the “frustratingly poor” accounting standards and handle “new stuff” and “new complexities to existing stuff” in a sensible a was as possible.

- There is no way that a computer is ever going to be able to handle #7 above.

- There is value if a computer can effectively do the “obvious stuff” or stuff where known good practices exists and can be leveraged, guide average accountants to do better and let good accountants focus on the highest value stuff.

- If software is created to help accountants perform the tasks and processes necessary to do all of the above, that software will have value.

And so, the value of an expert system for creating financial reports is to augment the skills of an accountant much like a calculator augments an accountant's capability to do math. If an accountant is freed from the task of checking all mathematical relations and obvious repetitive mechanical tasks; then accountants can focus on what they do best which is their judgement where that judgement is needed. The impact on the skills of accountants will be to move the bell shaped curve such: (more meet expectations, more are above expectations, and more are excellent)

Accountants will be better, financial reporting standards will be better, and financial report quality will be improved. The

universal technology of accountancy will be improved, and capital markets will function just a little better.

* * *

Human intelligence is one of the most valuable resources an organization can have; but at the same time human intelligence is very expensive because it is costly to create. As a result, accessing high-quality professional services, such as accounting and audit services, comes with a hefty price tag because gaining the skills and experience necessary to deliver those services is time consuming and expensive. However, a portion of the work these expensive skilled and experienced professionals deliver is mindless, repetitive grunt work. A good portion of the skills and experience relates to memorizing information. What if there was a way to effectively offload some of this mindless grunt work to a machine; enabling humans to focus on what only humans can do and tasks/processes machines have no chance of completing effectively? Not targeting hard, or impossible, to achieve human level intelligence, rather the

more easily achievable machine level of intelligence. Think of how a calculator is beneficial to an accountant. What if you could push on the bell shaped curve of expertise making average accountants and auditors better?

Imagine an ecosystem that would grow and evolve over time in many ways that create compounding value as opposed to increasing complexity. Priming this pump to get it up and running will be challenging and expensive, but the benefits of such a system will be very high. And this is not about bolting on something to an existing process, this is about a true transformation of processes and tasks; this is a paradigm shift.

Additional resources:

Comments

Post a Comment