The Threat of Inaccuracy

"The Threat of Inaccuracy". I wish that I could say I came up with that phrase, but I did not. That phrase is from a whitepaper published by Fluree, Decentralized Knowledge Graphs Enable Most Accurate Generative AI Results.

Effectively, what that whitepaper says is, "Garbage in, garbage out." How is artificial intelligence going to deal with inaccurate information?

Think about something. Why would you expect information provided by artificial intelligence, generative or otherwise, to be useful if there underlying input information has inaccuracies?

Things like workflow automation are a result of or consequence of the capability to remove inaccuracies from input information. And notice that I am using the term "information" and not "data".

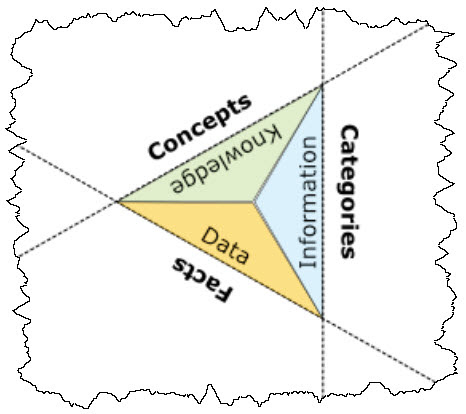

People don't seem to be grasping that what is happening is a paradigm shift. "Data", "information", and "knowledge" are not the same thing. Information is application independent, data is not.

(above graphic from EA Symbolic Twins)

When I begin my career as an auditor at Price Waterhouse, audit working papers were 100% paper-based. We literally created massive spreadsheets on paper. Machines could not read those paper-based audit working papers at all.

I don't know when what is now PWC went to fully electronic working papers. The transition from paper-based to fully electronic audit working papers (and accounting schedules of those being audited) was a gradual process over the past few decades. Many professional services firms such as PWC began adopting electronic audit working paper systems for workpaper preparation and review in the early 2000s. By the mid-2000s, a significant number of firms had implemented these systems to improve efficiency and effectiveness.

The transition wasn’t without challenges. Auditors faced difficulties in navigating the electronic systems and adapting to new workflows. Despite these challenges, the move to electronic audit working papers has become more widespread, with most firms now using electronic systems as the standard practice.

The American Institute of Certified Public Accountants (AICPA) is already contemplating audit automation; for example, see this paper, The Data-Driven Audit: How Automation and AI are Changing the Audit and the Role of the Auditor.

But notice how the AICPA used the term "Data-Driven" rather than "Information-Driven". Also, I doubt the AICPA is contemplating semantic oriented audit working papers as contrast to the current presentation oriented electronic audit working papers.

My personal bet is that accounting and audit working papers are going to be semantic oriented, leverage global standards, and machine readable, probably sooner than you might believe. Think modern semantic spreadsheets used to create accounting schedules and audit working papers.

The biggest issue is not creating semantic oriented spreadsheets; the primary problem is that most business information systems are a mess. Existing business information systems need to be fixed before artificial intelligence can deliver value. Systems will likely evolve incrementally, potentially rather slowly perhaps.

Graph-type or graph-oriented databases are the future of databases. Relational databases are not going away any time soon, or probably/maybe ever. The most impressive graph-type or graph-oriented databases that I have heard about are TerminusDB, Fluree, TypeDB, SWI-Prolog. But there are many others to choose from. (See this.) RDF, particularly RDF-Star, is effectively a graph oriented technical syntax. For more information on RDF Star see: What is RDF Star? and

Additional Information:

Comments

Post a Comment