Assault on Poor Financial Hygiene in XBRL-based Financial Statements

Many people have been complaining about the quality of XBRL-based digital financial statements submitted to the SEC for many years. XBRL US even formed a Data Quality Committee to address quality issues.

ESEF XBRL-based financial statements submitted to the ESMA are now being scrutinized and seen to also contain quality issues. See this report which looks at ESEF report quality by audit firm and this ESEF observatory.

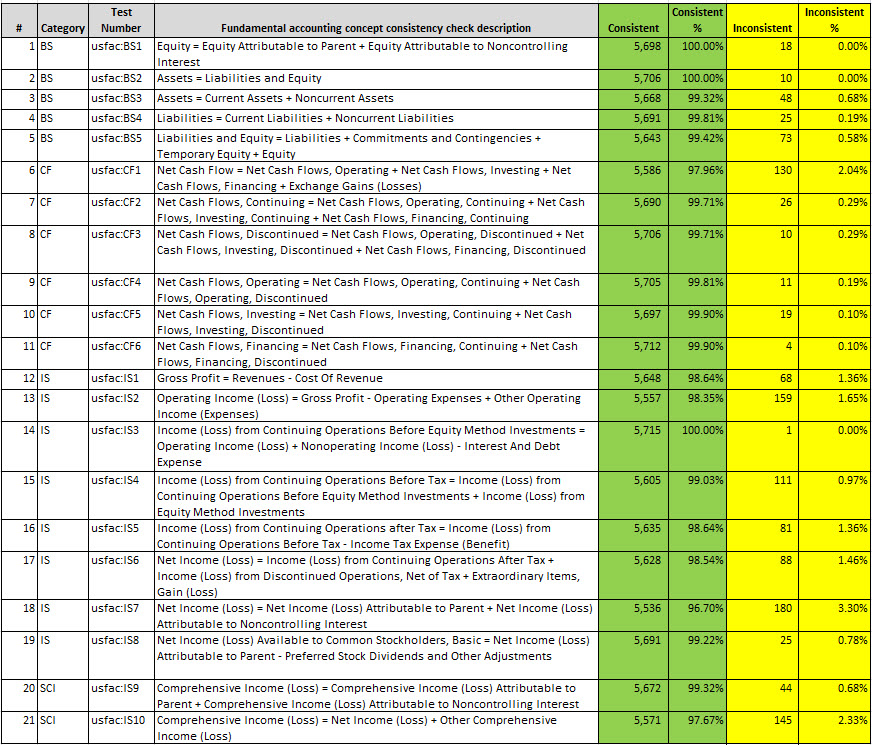

Myself and a handful of others (like XBRLogic) have been measuring the quality of XBRL-based financial statements that have been submitted to the SEC for a number of years. I have personally looked at the high-level fundamental relationships between financial concepts and their relations between 2013 and 2018. What I saw was many mistakes, improvements over time, but my last measurement showed that about 90% of reports were free from these high-level mistakes, but that means that about 10% of reports had some sort of error. Here is a summary of my last measurement: (click here)

Here is how to read that table. Look at row #2. That row shows the rule "Assets = Liabilities and Equity", a fundamental rule in accounting referred to as the accounting equation. Of the 5,716 reports that I measured (all the 10-Ks submitted to the SEC for fiscal year 2018); 5,706 of those reports were consistent with that fundamental accounting rule; but there were 10 that were not consistent and I manually confirmed that each of those 10 reports were, in fact, in error.

Now, the 10 reports that had that mistake in 2018 was an improvement from the 53 reports that had that mistake, again confirmed by me manually, when I made my first measurements in 2013.

Yes, I am saying that there were 10 public companies that reported balance sheets that did not balance within the set of 5,716 10-Ks submitted to the SEC for fiscal year ended 2018. That table above lays out other similar mistakes, again all confirmed manually to actually be an error made by the reporting public company or whoever created the XBRL-based financial report that was submitted.

Within the DOW 30 companies, measurements in 2022 revealed that there were 4 specific confirmed high-level accounting concept errors. Again, all four errors were confirmed manually by me personally to be errors. Within the Fortune 100 (which includes the DOW 30), measurements in 2022 revealed 17 specific errors. Likewise, these were manually confirmed by me to actually be reporting mistakes.

So what is my point here? Well, I have several points:

- Understanding these errors and how the errors occur can help reporting entities creating XBRL-based reports better understand those reports and avoid these sorts of errors.

- Data aggregators spend about 90% of their software development effort when trying to make use of all that XBRL-based financial information overcoming these sorts of errors in reported information. I have talked to many of these data aggregators.

- XBRL-based reporting can in fact work. But regulators like the SEC and ESMA need to provide verification walls that check the quality of reports before they accept a submitted report.

- The fundamental accounting concepts and the relations between those concepts is not the only thing that needs to be checked. Poking and prodding of XBRL-based reports has revealed a hand full of things which I refer to as the "pillars of quality" which reports need to have in order to be fundamentally usable.

- My "pillars of quality" do not guarantee that everything in the submitted XBRL-based report is correct; they only check, to the extent that machine-readable rules are provided, to make sure specific things are NOT WRONG. Basically, all my rules are NECESSARY but they are not SUFFICIENT. You can never really guarantee that everything is right, you can only prove what is wrong to the extent of the machine-readable rules that are provided.

- XBRL-based reports submitted to both the SEC and ESMA have very similar issues. XBRL-based reporting has been occurring since 2010. Seems like quality could be dialed in by now.

- The same rules necessary for verifying that reports are prepared correctly are the rules necessary to extract information from those XBRL-based reports effectively. Financial reports are not, and should not, be forms. Those financial reports are knowledge graphs. Because the financial reporting rules allow for the use of different subtotals and totals and the use of different line items (i.e. XBRL concepts) to report information; those validation rules are required to extract information from the reports effectively. For example, many different concepts might be used to report the line item "revenues". That list of possible concepts is necessary to effectively extract information from those reports.

- Financial Statements Designed to be Analyzed

- Achieving trust and efficient financial reporting through XBRL (PWC)

- HOW SBRM ENABLES DIGITAL ASSET WHITE PAPER COMPLIANCE UNDER THE EU'S MICA REGULATIONS

- Inaccuracies in Earnings Per Share in IFRS in Europe (LinkedIn)

- Inaccuracies in Earnings Per Share in IFRS in Europe (PDF)

- Auditchain Pacioli Validation Results (Demonstration on Fortune 100)

- Pacioli AI Logic and Rules Engine

Comments

Post a Comment